The LoneStar 529 Plan® is an advisor-sold IRC Sec. 529 education savings plan. The Texas Prepaid Higher Education Tuition Board maintains and administers the plan. Participation in the tax-advantaged plan is available to all U.S. citizens or permanent resident aliens at least 18 years old with a valid Social Security number regardless of income or state of residence. The

Plan:

The LoneStar 529 Plan, which is a 529 Plan.

is managed by Orion Advisor Solutions, Inc. You will be required to designate a

Financial Advisor:

Any individual or entity that is appropriately licensed and who has entered into an agreement with the Plan Distributor to distribute Savings Trust Agreements and interests in the Plan represented by Accounts to public investors. This term may include brokers and financial intermediaries such as investment advisors or banks.

on your

Application:

The LoneStar 529 Plan® enrollment form used to collect eligibility information and establish an Account.

when you enroll in the plan. A financial advisor is any individual or entity that is appropriately licensed and who has entered into an agreement with the plan distributor to distribute interests in the plan. This term may include brokers, and financial intermediaries, such as investment advisors or banks.

Some states offer favorable tax treatment to their residents only if they invest in the state’s own plan. Non-residents of Texas should consider whether their state offers its residents a

529 Plan:

A state-sponsored, tax-advantaged college savings program established under and operated in accordance with IRC §529 to help save for Qualified Higher Education Expenses.

with alternative tax advantages.

Why Choose this Plan?

No matter how big an adventure your child chooses to embark on, the LoneStar 529 Plan can help you save for the education they need.

Tailored Investments from Trusted Industry Leaders

The LoneStar 529 Plan offers a wide range of investment options managed by industry leaders, Artisan, Baird, DFA, Dodge & Cox, Eaton Vance, Federated Hermes, Neuberger Berman, New York Life, PIMCO, T. Rowe Price, and Vanguard.

You can choose among a variety of investment strategies depending on your risk tolerance, time horizon, financial situation and other variables.

Low Investment Minimums and High Maximums

Open a LoneStar 529 Plan with as little as $25 (or $15 if funded through an

Automatic Investment Plan (AIP):

Contributions to your Account in a fixed amount of money in regular intervals. Funds are automatically deducted from the Account Owner’s bank account or other financial institution, or through payroll deductions. 2) and contribute up to $500,0001 per

Beneficiary:

The individual identified by the Account Owner whose Qualified Higher Education Expenses are expected to be paid from the Account or, for Accounts owned by a state or local government or qualifying tax-exempt organization (otherwise known as a 501(c)(3) entity) as part of its operation of a scholarship program, the recipient of a scholarship whose Qualified Higher Education Expenses are expected to be paid from the Account. Any individual may be the Beneficiary of an Account, including the Account Owner.A government entity or 501(c)(3) not-for-profit organization can establish an Account to fund scholarship programs without designating a Beneficiary at the time the Account is established.

To ensure maximum savings, the

Plan:

The LoneStar 529 Plan, which is a 529 Plan.

offers an Automatic Investment Plan (AIP).2 Choose the amount and frequency of contributions, and we take care of the rest!

The Ease of Online Account Maintenance

Once you open your

Account:

A savings trust account established by an Account Owner pursuant to the Savings Trust Agreement for purposes of investing in one or more portfolios. Accounts are part of the Plan and are held in the name of the Plan on behalf of and for the benefit of the Account Owners and the Beneficiaries.

after consulting with your

Financial Advisor:

Any individual or entity that is appropriately licensed and who has entered into an agreement with the Plan Distributor to distribute Savings Trust Agreements and interests in the Plan represented by Accounts to public investors. This term may include brokers and financial intermediaries such as investment advisors or banks.

on the investment options, you can manage your account online at your convenience, make changes to investment options, and handle other account maintenance tasks such as changing a

Beneficiary:

The individual identified by the Account Owner whose Qualified Higher Education Expenses are expected to be paid from the Account or, for Accounts owned by a state or local government or qualifying tax-exempt organization (otherwise known as a 501(c)(3) entity) as part of its operation of a scholarship program, the recipient of a scholarship whose Qualified Higher Education Expenses are expected to be paid from the Account. Any individual may be the Beneficiary of an Account, including the Account Owner.A government entity or 501(c)(3) not-for-profit organization can establish an Account to fund scholarship programs without designating a Beneficiary at the time the Account is established.

1. Additional contributions to your

Account:

A savings trust account established by an Account Owner pursuant to the Savings Trust Agreement for purposes of investing in one or more portfolios. Accounts are part of the Plan and are held in the name of the Plan on behalf of and for the benefit of the Account Owners and the Beneficiaries.

will be rejected if it would cause the aggregate contribution balance of all Texas 529 program accounts for your

Beneficiary:

The individual identified by the Account Owner whose Qualified Higher Education Expenses are expected to be paid from the Account or, for Accounts owned by a state or local government or qualifying tax-exempt organization (otherwise known as a 501(c)(3) entity) as part of its operation of a scholarship program, the recipient of a scholarship whose Qualified Higher Education Expenses are expected to be paid from the Account. Any individual may be the Beneficiary of an Account, including the Account Owner.A government entity or 501(c)(3) not-for-profit organization can establish an Account to fund scholarship programs without designating a Beneficiary at the time the Account is established.

to exceed the

Maximum Texas Program Contribution Limit:

The maximum contribution balance (currently $500,000 per Board approval) per Beneficiary aggregated across all accounts in Texas‑sponsored 529 Plans that cannot be exceeded through additional contributions. Accounts that have reached the limit may continue to accrue earnings, but additional contributions are prohibited.

which is currently $500,000. This limit considers all 529 programs administered by Texas—the LoneStar 529 Plan, the Texas Guaranteed Tuition Plan, the Texas Tuition Promise Fund®, and the Texas College Savings Plan®—regardless of the owner(s) of the account(s). New contributions will not be allowed once this limit is reached, but earnings will continue to accrue. Consult your tax advisor for information on how 529 tax treatments would apply to your particular situation.

2. Automatic investing does not assure a profit and does not protect against loss in declining markets. Before investing, investors should evaluate their long-term financial ability to participate in such a plan.

Features

Tax-free Growth

Earnings in the

Plan:

The LoneStar 529 Plan, which is a 529 Plan.

grow federal income tax free for the life of the

Account:

A savings trust account established by an Account Owner pursuant to the Savings Trust Agreement for purposes of investing in one or more portfolios. Accounts are part of the Plan and are held in the name of the Plan on behalf of and for the benefit of the Account Owners and the Beneficiaries.

.

Tax-free Withdrawal

You can withdraw the money federal tax free, as long as it’s used to pay for

Qualified Higher Education Expenses:

Undergraduate and graduate tuition, fees, books, supplies, and equipment required for a Beneficiary’s enrollment or attendance at an Eligible Educational Institution. The term includes computers and peripherals, software (except for non-educational sports, games, or hobby software), and internet service if used primarily by the Beneficiary while enrolled at an Eligible Educational Institution. Expenses for special needs services incurred in connection with enrollment or attendance at an Eligible Educational Institution are also included in the definition. The term also includes reasonable room and board for beneficiaries who are enrolled at least half-time at an Eligible Educational institution

Qualifying expenses also include fees, books, supplies, and equipment necessary to participate in a registered apprenticeship program, and the ability to repay up to $10,000 (lifetime per student) in student loans for the Beneficiary or the Beneficiary’s sibling. Additionally, 529 Plans may be used for K-12 tuition for private, public, or religious school (up to $10,000 per year per Beneficiary).

Recent tax reform legislation changes allowing for payment of K-12 tuition were on a federal level, and the tax consequences of using 529 plans for elementary or secondary education tuition expenses will vary depending on state law and may include recapture of tax deductions received from the original state as well as penalties. The account owner should consult with a tax or legal advisor before using the plan for K-12 tuition.

When withdrawals are used for other purposes (a non-qualified withdrawal), the earnings portion of the withdrawal is subject to federal income taxes, and an additional 10% federal tax and for non-Texas residents, any applicable state income tax.

Use Your Savings at Schools in the U.S. and Abroad

You can use your savings to pay for

Qualified Higher Education Expenses:

Undergraduate and graduate tuition, fees, books, supplies, and equipment required for a Beneficiary’s enrollment or attendance at an Eligible Educational Institution. The term includes computers and peripherals, software (except for non-educational sports, games, or hobby software), and internet service if used primarily by the Beneficiary while enrolled at an Eligible Educational Institution. Expenses for special needs services incurred in connection with enrollment or attendance at an Eligible Educational Institution are also included in the definition. The term also includes reasonable room and board for beneficiaries who are enrolled at least half-time at an Eligible Educational institution

Qualifying expenses also include fees, books, supplies, and equipment necessary to participate in a registered apprenticeship program, and the ability to repay up to $10,000 (lifetime per student) in student loans for the Beneficiary or the Beneficiary’s sibling. Additionally, 529 Plans may be used for K-12 tuition for private, public, or religious school (up to $10,000 per year per Beneficiary).

Recent tax reform legislation changes allowing for payment of K-12 tuition were on a federal level, and the tax consequences of using 529 plans for elementary or secondary education tuition expenses will vary depending on state law and may include recapture of tax deductions received from the original state as well as penalties. The account owner should consult with a tax or legal advisor before using the plan for K-12 tuition.

at most accredited institutions in the U.S., including career schools, two- and four-year colleges and universities, as well as at some foreign institutions.

Because the 529

Account:

A savings trust account established by an Account Owner pursuant to the Savings Trust Agreement for purposes of investing in one or more portfolios. Accounts are part of the Plan and are held in the name of the Plan on behalf of and for the benefit of the Account Owners and the Beneficiaries.

is in your name, you retain control over when and how the savings are used. You decide when and how much to contribute, and control when to make withdrawals.

You can even change

Beneficiary:

The individual identified by the Account Owner whose Qualified Higher Education Expenses are expected to be paid from the Account or, for Accounts owned by a state or local government or qualifying tax-exempt organization (otherwise known as a 501(c)(3) entity) as part of its operation of a scholarship program, the recipient of a scholarship whose Qualified Higher Education Expenses are expected to be paid from the Account. Any individual may be the Beneficiary of an Account, including the Account Owner.A government entity or 501(c)(3) not-for-profit organization can establish an Account to fund scholarship programs without designating a Beneficiary at the time the Account is established.

among qualified family members without penalty or tax ramifications.

Broad Range of Investment Options

The LoneStar 529 Plan lets you pick your path to investing by offering numerous investment portfolios based on risk tolerance, time horizon and financial situation. It’s easy to find one that suits your particular needs.

Use Your 529 Account for K-12 Tuition, Student Loan Repayment or Participation in a registered apprenticeship program

Under

Section 529:

Section 529 of the Internal Revenue Code specifies the requirements for qualified tuition programs (529 Plans).

of the Internal Revenue

Code, or IRC:

The Internal Revenue Code of 1986, as amended.

assets in the

Account:

A savings trust account established by an Account Owner pursuant to the Savings Trust Agreement for purposes of investing in one or more portfolios. Accounts are part of the Plan and are held in the name of the Plan on behalf of and for the benefit of the Account Owners and the Beneficiaries.

can also be withdrawn on a tax-free basis for any of the following purposes:

Fees, books, supplies and equipment required for the participation of a designated beneficiary in a Registered Apprenticeship Program;

up to $10,000 per year of tuition in connection with enrollment or attendance at an elementary or secondary public, private or religious school as determined under applicable state law1; and

up to $10,000 in amounts paid as principal or interest on any Qualified Education Loan of the designated beneficiary or a sibling of the designated beneficiary.

The $10,000 limitation for public, private, or religious schools applies on a per-student basis, rather than a per-account basis; therefore, a maximum of $10,000 may be funded from all 529 accounts combined for one beneficiary. Similarly, the $10,000 aggregate limitation on Qualified Education Loan Repayments applies on a per-student basis regardless of whether the funds are distributed from multiple accounts.

Before making contributions or withdrawals from the

Plan:

The LoneStar 529 Plan, which is a 529 Plan.

for qualified expenses at K-12 schools, registered apprenticeship programs, or qualified education loan repayments,

Account Owner:

The individual or entity signing the Application and establishing an Account or any successor to such individual or entity. References in this Glossary to “you” or “your” mean the Account Owner in such capacity.

should consider that (i) the Investment Portfolios within the Plan were designed for college savers (e.g., persons saving for undergraduate and graduate school) not saving for qualified expenses at K-12 schools, registered apprenticeship programs, or qualified education loan repayments, and therefore Account Owners should take into consideration their investment horizon, and (ii) the information presented is based on a good faith interpretation of the statutory language.

1. Recent tax reform legislation changes allowing for payment of K-12 tuition were on a federal level, and the tax consequences of using

529 Plan:

A state-sponsored, tax-advantaged college savings program established under and operated in accordance with IRC §529 to help save for Qualified Higher Education Expenses.

for elementary or secondary education tuition expenses will vary depending on state law and may include recapture of tax deductions received from the original state as well as penalties. The

Account Owner:

The individual or entity signing the Application and establishing an Account or any successor to such individual or entity. References in this Glossary to “you” or “your” mean the Account Owner in such capacity.

should consult with a tax or legal advisor before using the

Plan:

The LoneStar 529 Plan, which is a 529 Plan.

for K-12 tuition.

Tax Incentives

Anyone can benefit from the tax advantages of the LoneStar 529 Plan, regardless of income level, tax bracket or financial situation.

Tax-free Withdrawal

You can withdraw funds in a

529 Plan:

A state-sponsored, tax-advantaged college savings program established under and operated in accordance with IRC §529 to help save for Qualified Higher Education Expenses. Account:

A savings trust account established by an Account Owner pursuant to the Savings Trust Agreement for purposes of investing in one or more portfolios. Accounts are part of the Plan and are held in the name of the Plan on behalf of and for the benefit of the Account Owners and the Beneficiaries.

to pay for

Qualified Higher Education Expenses:

Undergraduate and graduate tuition, fees, books, supplies, and equipment required for a Beneficiary’s enrollment or attendance at an Eligible Educational Institution. The term includes computers and peripherals, software (except for non-educational sports, games, or hobby software), and internet service if used primarily by the Beneficiary while enrolled at an Eligible Educational Institution. Expenses for special needs services incurred in connection with enrollment or attendance at an Eligible Educational Institution are also included in the definition. The term also includes reasonable room and board for beneficiaries who are enrolled at least half-time at an Eligible Educational institution

Qualifying expenses also include fees, books, supplies, and equipment necessary to participate in a registered apprenticeship program, and the ability to repay up to $10,000 (lifetime per student) in student loans for the Beneficiary or the Beneficiary’s sibling. Additionally, 529 Plans may be used for K-12 tuition for private, public, or religious school (up to $10,000 per year per Beneficiary).

Recent tax reform legislation changes allowing for payment of K-12 tuition were on a federal level, and the tax consequences of using 529 plans for elementary or secondary education tuition expenses will vary depending on state law and may include recapture of tax deductions received from the original state as well as penalties. The account owner should consult with a tax or legal advisor before using the plan for K-12 tuition.

without incurring federal taxes.

Using account assets for any other purpose would likely be subject to federal income tax on any earnings as well as an additional federal tax of 10% and, for non-Texas residents, any applicable state income taxes. The state income tax consequences will vary by state, but there would be no impact in Texas because the state does not impose an income tax on individuals.

Recent tax reform legislation changes allowing for payment of K-12 tuition were on a federal level, and the tax consequences of using

529 Plan:

A state-sponsored, tax-advantaged college savings program established under and operated in accordance with IRC §529 to help save for Qualified Higher Education Expenses.

for elementary or secondary education tuition expenses will vary depending on state law and may include recapture of tax deductions received from the original state as well as penalties. The

Account Owner:

The individual or entity signing the Application and establishing an Account or any successor to such individual or entity. References in this Glossary to “you” or “your” mean the Account Owner in such capacity.

should consult with a tax or legal advisor before using the

Plan:

The LoneStar 529 Plan, which is a 529 Plan.

for K-12 tuition.

Tax-free Growth

Earnings in

529 Plan:

A state-sponsored, tax-advantaged college savings program established under and operated in accordance with IRC §529 to help save for Qualified Higher Education Expenses.

are not subject to federal or state taxes as assets in the

Account:

A savings trust account established by an Account Owner pursuant to the Savings Trust Agreement for purposes of investing in one or more portfolios. Accounts are part of the Plan and are held in the name of the Plan on behalf of and for the benefit of the Account Owners and the Beneficiaries.

grow and if used for

Qualified Higher Education Expenses:

Undergraduate and graduate tuition, fees, books, supplies, and equipment required for a Beneficiary’s enrollment or attendance at an Eligible Educational Institution. The term includes computers and peripherals, software (except for non-educational sports, games, or hobby software), and internet service if used primarily by the Beneficiary while enrolled at an Eligible Educational Institution. Expenses for special needs services incurred in connection with enrollment or attendance at an Eligible Educational Institution are also included in the definition. The term also includes reasonable room and board for beneficiaries who are enrolled at least half-time at an Eligible Educational institution

Qualifying expenses also include fees, books, supplies, and equipment necessary to participate in a registered apprenticeship program, and the ability to repay up to $10,000 (lifetime per student) in student loans for the Beneficiary or the Beneficiary’s sibling. Additionally, 529 Plans may be used for K-12 tuition for private, public, or religious school (up to $10,000 per year per Beneficiary).

Recent tax reform legislation changes allowing for payment of K-12 tuition were on a federal level, and the tax consequences of using 529 plans for elementary or secondary education tuition expenses will vary depending on state law and may include recapture of tax deductions received from the original state as well as penalties. The account owner should consult with a tax or legal advisor before using the plan for K-12 tuition.

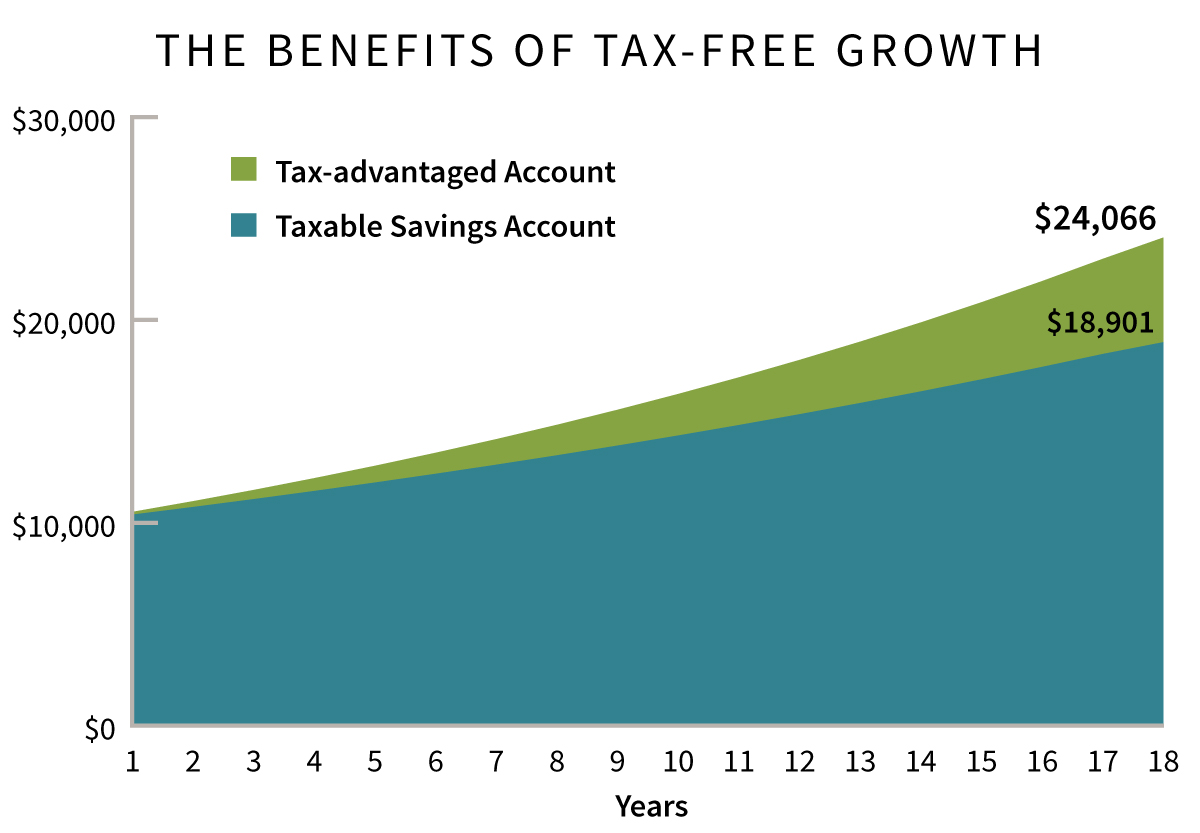

As the chart below shows, the tax advantages of a 529 plan could mean the difference between funding a higher education and coming up short.

This hypothetical illustration assumes an initial investment of $10,000 and a 5%

Annual Rate of Return:

The rate of return on your investment, expressed as a percentage of the total amount invested.

. The taxable account assumes a 28% federal tax rate. The illustration does not represent the performance of any specific account or investment and does not reflect any plan fees or charges that may apply. If such fees or charges were taken into account, returns would have been lower.

Gift and Estate Tax Planning Benefits

In recognition of the importance of saving for

Qualified Higher Education Expenses:

Undergraduate and graduate tuition, fees, books, supplies, and equipment required for a Beneficiary’s enrollment or attendance at an Eligible Educational Institution. The term includes computers and peripherals, software (except for non-educational sports, games, or hobby software), and internet service if used primarily by the Beneficiary while enrolled at an Eligible Educational Institution. Expenses for special needs services incurred in connection with enrollment or attendance at an Eligible Educational Institution are also included in the definition. The term also includes reasonable room and board for beneficiaries who are enrolled at least half-time at an Eligible Educational institution

Qualifying expenses also include fees, books, supplies, and equipment necessary to participate in a registered apprenticeship program, and the ability to repay up to $10,000 (lifetime per student) in student loans for the Beneficiary or the Beneficiary’s sibling. Additionally, 529 Plans may be used for K-12 tuition for private, public, or religious school (up to $10,000 per year per Beneficiary).

Recent tax reform legislation changes allowing for payment of K-12 tuition were on a federal level, and the tax consequences of using 529 plans for elementary or secondary education tuition expenses will vary depending on state law and may include recapture of tax deductions received from the original state as well as penalties. The account owner should consult with a tax or legal advisor before using the plan for K-12 tuition.529 Plan:

A state-sponsored, tax-advantaged college savings program established under and operated in accordance with IRC §529 to help save for Qualified Higher Education Expenses.

qualify for special gift tax exclusion. You can contribute up to $17,000 ($34,000 for married couples) annually per

Beneficiary:

The individual identified by the Account Owner whose Qualified Higher Education Expenses are expected to be paid from the Account or, for Accounts owned by a state or local government or qualifying tax-exempt organization (otherwise known as a 501(c)(3) entity) as part of its operation of a scholarship program, the recipient of a scholarship whose Qualified Higher Education Expenses are expected to be paid from the Account. Any individual may be the Beneficiary of an Account, including the Account Owner.A government entity or 501(c)(3) not-for-profit organization can establish an Account to fund scholarship programs without designating a Beneficiary at the time the Account is established.

or up to $85,000 ($170,000 for married couples) prorated over a five-year period—without taxes.1

Keep in mind that your contributions are excluded from your estate.

Scholarship Withdrawals

Funds may be withdrawn without penalty if the

Beneficiary:

The individual identified by the Account Owner whose Qualified Higher Education Expenses are expected to be paid from the Account or, for Accounts owned by a state or local government or qualifying tax-exempt organization (otherwise known as a 501(c)(3) entity) as part of its operation of a scholarship program, the recipient of a scholarship whose Qualified Higher Education Expenses are expected to be paid from the Account. Any individual may be the Beneficiary of an Account, including the Account Owner.A government entity or 501(c)(3) not-for-profit organization can establish an Account to fund scholarship programs without designating a Beneficiary at the time the Account is established.

receives a scholarship (up to the scholarship amount), or in the event of the death or disability of the beneficiary. However, ordinary federal income tax and any applicable state income tax would be owed on any investment earnings.

1. If the

Account Owner:

The individual or entity signing the Application and establishing an Account or any successor to such individual or entity. References in this Glossary to “you” or “your” mean the Account Owner in such capacity.

utilizes the special five-year lump sum exclusion and dies within five years of the funding date, the portion of the contribution allocable to the years remaining in the five-year period (beginning with the year after the Account Owner’s death) would be included in the account owner’s estate for Federal estate tax purposes. Clients should consult their tax advisor.